Contact us

Contact us

Business Bay, Opal tower, Office 1301, Dubai, United Arab Emirates.

Office time: 9:00 – 18:00

Business Bay, Opal tower, Office 1301, Dubai, United Arab Emirates.

Office time: 9:00 – 18:00

+ 971 58 515 7428

+ 971 58 515 7428

Contact us

Business Bay, Opal tower, Office 1301, Dubai, United Arab Emirates.

Office time: 9:00 – 18:00

+ 971 58 515 7428

Contact us

Business Bay, Opal tower, Office 1301, Dubai, United Arab Emirates.

Office time: 9:00 – 18:00

+ 971 58 515 7428

In this article, I will continue discussing potential areas of creative accounting, now in regards to expenses.

In my opinion, revenues are the usual area of inflation and the most obvious one. When analyzing company’s operations, most investors and analytics usually expect the sales growth and therefore meeting these expectations of sales growth is the most challenging area for the company’s management. Expected sales growth is usually number one indicator for picking stock in portfolio.

Meanwhile creativity with accounting for expenses usually takes place when the companies need to sustain net earnings growth or simply show positive earnings.

The ways to be creative with expenses are so multiple that it can take a book to write.

Below I will bring a three interesting cases of creativity and significant judgement with expenses based on examples of public companies, including

1. Overcapitalization of the normal operating expenses

The most notable case, which could be presented, was that of WorldCom. In mid-1990s this large telecommunication company signed long-term network access arrangements to lease line capacity from other telecommunication carriers. These contracts included fees that WorldCom paid for the right to use other companies’ telecommunication networks to connect calls and were at first accounted by WorldCom as an expense.

However, soon when the revenue growth started to lag behind the analysts’ expectations, the company decided to increase profitability by a simple change in accounting policies. Instead of expensing the line costs, the company changed its accounting policy to capitalizing the line costs. The company decreased its operating costs and inflated its non-current assets. For instance, only in the 4th quarter 2001 the Worldcom officers fraudulently made entries in WorldCom's general ledger, which effectively erased approximately $941 million from its line cost expenses for the fourth quarter of 2001 and correspondingly increased capital asset accounts.

The summary of the misstatements is presented below.

|

Filed |

Reported Line |

Reported Income |

Actual Line |

Actual Income |

|

10-Q, 3rd Q. 2000 |

$3.867 billion |

$1.736 billion |

$4.695 billion |

$908 million |

|

10-K, 2000 |

$15.462 billion |

$7.568 billion |

$16.697 billion |

$6.333 billion |

|

10-Q, 1st Q. 2001 |

$4.108 billion |

$988 million |

$4.879 billion |

$217 million |

|

10-Q, 2nd Q. 2001 |

$3.73 billion |

$159 million |

$4.29 billion |

$401 million loss |

|

10-Q, 3rd Q. 2001 |

$3.745 billion |

$845 million |

$4.488 billion |

$102 million |

|

10-K, 2001 |

$14.739 billion |

$2.393 billion |

$17.754 billion |

$622 million loss |

|

10-Q, 1st Q. 2002 |

$3.479 billion |

$240 million |

$4.297 billion |

$578 million loss |

The fraud was unraveled in 2002 as a result of routine internal audit and led to bankruptcy of the company, 25-year jail sentence to the company’s CEO and even to introduction of new Sarbanes-Oxley (SOX) legislation in the USA. The latter was introduced to enhance corporate accountability and strengthen financial reporting requirements. SOX imposed stricter regulations on public companies, including the establishment of independent audit committees and increased oversight of financial reporting.

2. Amortizing assets too slow

The next obvious way to inflate profits is lower than needed depreciation of assets by extending the useful life of a non-current asset. Useful lives are accounting estimates and can be changed by the management in any time without even sometimes presenting the detailed information on the change in the financial statements. Changes in accounting estimates do not require revision of the previous financial statements and should be applied prospectively.

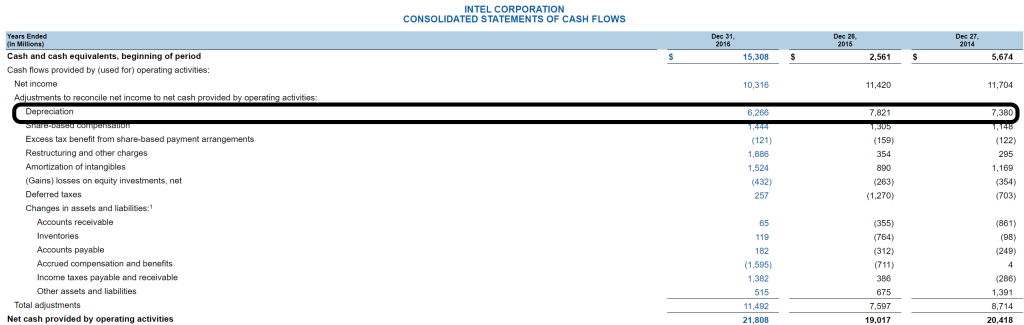

Let’s for example take a look at Intel’s financial statements for 2015. The company decided to increase useful lives of its machinery and equipment from four to five years bringing an additional $1.5 billion of lower depreciation and respectively higher profits in the next year of 2016. Below is an extract from the accounting policies of Intel presented in 2005 annual financial statements.

Property, Plant and Equipment Depreciation. Management judgment is required in determining the estimated economic useful lives of our property, plant and equipment, which can materially impact our depreciation expense. Accordingly, at least annually, we evaluate the period over which we expect to recover the economic value of these assets. During the assessment performed in Q4 2015, we considered factors such as the lengthening of the process technology cadence resulting in longer node transitions on both 14nm and 10nm products. With those longer transitions, we added a third product to our 14nm roadmap. We have also increased re-use of machinery and tools across each generation of process technology. As a result, we determined that the useful lives of machinery and equipment in our wafer fabrication facilities should be increased from four to five years. We will account for this as a change in estimate that will be applied prospectively, effective in Q1 2016. This change in depreciable life drives approximately $1.5 billion in lower depreciation expense for 2016. Approximately half of this benefit will increase gross margin (impacting both unit cost and start-up costs), approximately one-fourth will decrease R&D expenses, and the remaining one-fourth will result in lower inventory costs and ending inventory values.

As further can be seen in the financial statements for 2016 the single accounting trick added about 17% to the net earnings of Intel for 2016 and is quite obvious when analyzing the Intel’s financial statements for 2014-2016.

If we go further and compare the reporting to the Intel’s equity market prices it can be seen that the change in accounting estimates could be made to assist earnings in the situation of stagnating share prices during 2015.

3. Failing to impair non-current assets

For over 22 years of my experience in finance the issue of impairment is the most notable judgement the management of the companies should make every reporting period in almost any industry.

The applicable IAS 36 accounting standard requires all assets to be tested for impairment at the end of reporting period, which means comparing its recoverable value (which can delivered through either sale or continuing use) and book value (the value of the asset in the account).

The standard also requires to check if there are any indications of impairment prior to making the impairment test by reviewing external sources (declines in market value, negative changes in technology, markets, economy, or laws, increases in market interest rates and others) and internal sources of information (obsolescence or physical damage, worse economic performance than expected etc.). And mostly the companies do have any of indications, which require them carry-out the regular impairment testing.

The impairment test is usually conducted by analyzing the so called value in use, or net present value of net cash flows the asset (or groups of assets) would bring to the company. The impairment test is subject to a huge amount of assumptions on future prices, growth rates, discount rates etc., which can bring significantly different results.

Our firm, ADE Professional Solutions, had an experience of assisting multiple clients doing hundreds of impairment testing procedures. But the most prominent case in our expertise was consulting one of the clients, a largest electricity generation company, in simultaneous testing of its 90 power stations, each representing a separate CGU (cash-generating unit) based on 5 sets of assumptions on future prices and volumes of electricity to be produced and sold, growth in personnel and other costs, assumptions of discount rates etc. The results proved completely different picture of the business and applications for the company’s financial statements up to the full impairment of all assets. Just imagine 90 full-scope financial models re-evaluated under 5 different scenarios. It shows the impact the accounting judgements can have on the information presented to the investors.

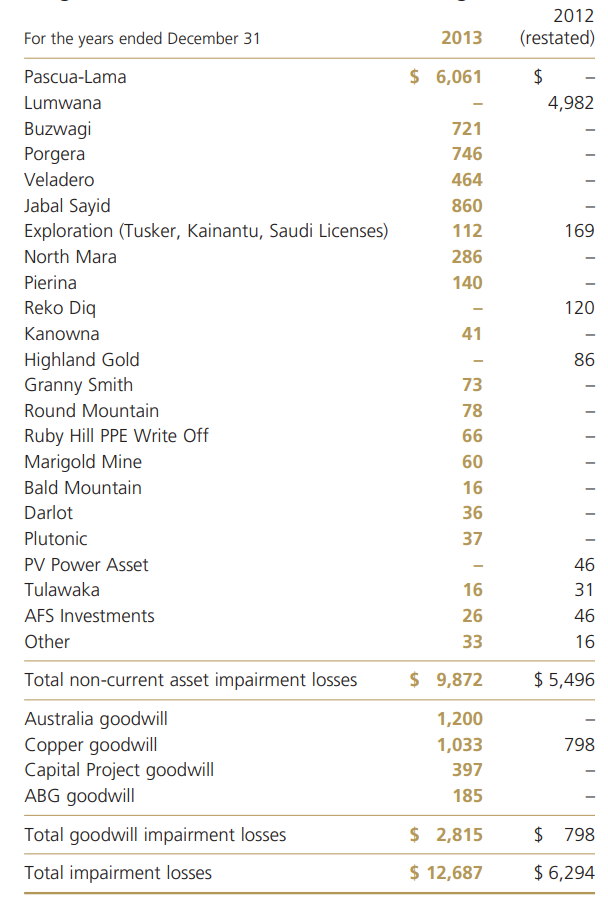

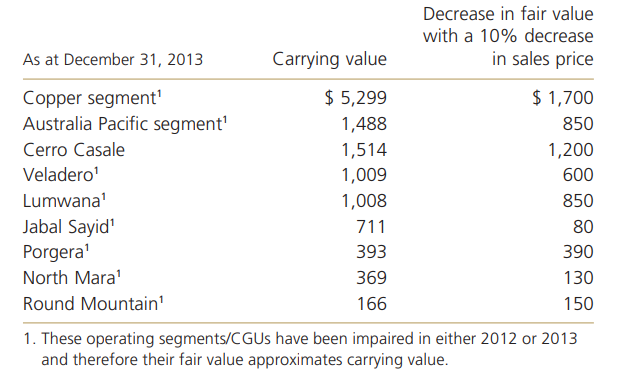

Let’s look at an example of a public company’s financial statements and analyze an example of Barrick Gold Corporation and its financial statements for 2013.

As can be seen in the consolidated income statements the company recognized an impairment of USD 12,687 in 2013, an amount higher than the company’s revenues from sales. If further analyzed, we see that the company decided in 2013 to clean its balance sheet and impair one third of its fixed assets and goodwill of $38,114 million as at December 31, 2012.

The impairment charge was mostly attributed to decline in forecasted market prices of gold, silver and copper, regulatory challenges and changes in mine plans.

The table below shows the list of the key assumptions the company made in analyzing value in use and the fact that a single 10% change on assumptions on sales prices would bring an additional impairment of USD 5,930 million of impairment charge.

This example shows how significant the impairment charges can be and the potential effect on the net earnings they may have.

I hope the examples would help the users of the financial statements better understand the focus areas and potential implication of the above-analyzed accounting issues on the financial statements.