The United Arab Emirates (UAE) has long been recognized as one of the most attractive jurisdictions for businesses due to its tax-friendly policies. However, in recent years, the UAE has been gradually aligning with global tax standards, introducing several key tax regulations to diversify revenue sources and strengthen its position in the international economic environment.

One of the most significant tax reforms took place in 2023 with the introduction of corporate income tax (CIT). This has reshaped the financial and operational landscape for businesses, particularly in industries such as real estate, construction, and trade.

This guide provides a comprehensive overview of the UAE tax system, highlighting the most relevant taxes and the implications of corporate tax for businesses.

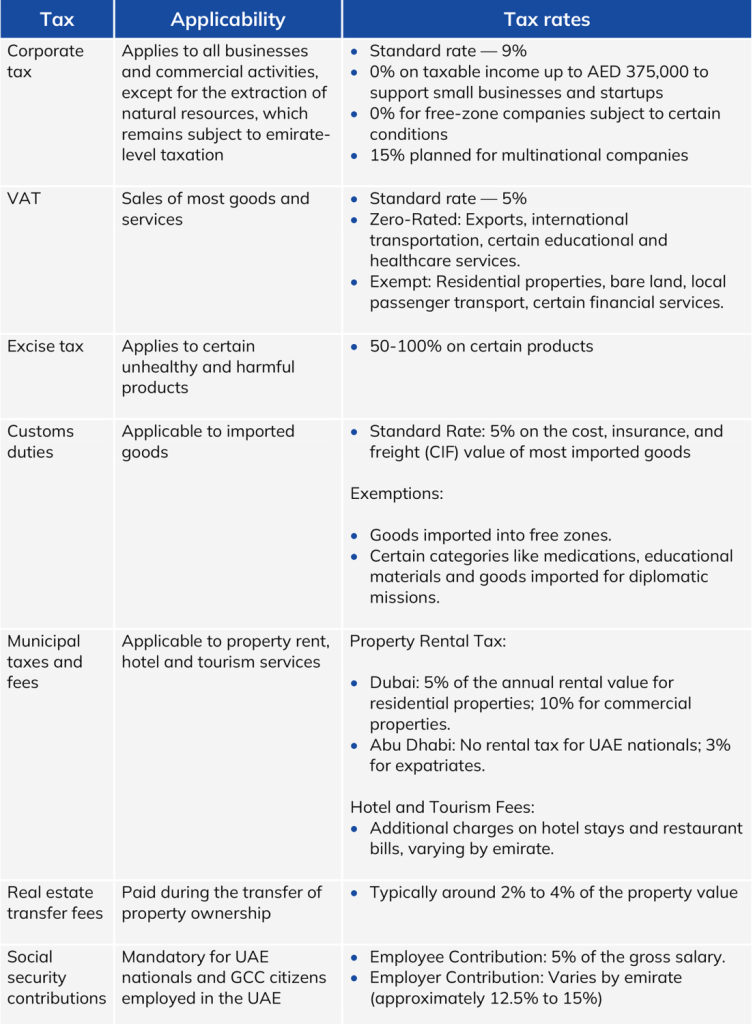

The table below outlines the key taxes applicable in the UAE:

The introduction of corporate income tax (CIT) represents a major shift in the UAE’s tax policy, directly affecting businesses across various industries. While the 9% tax rate remains relatively low compared to global standards, it still introduces new financial and administrative challenges for companies operating in the UAE.

Here’s a detailed breakdown of how corporate tax impacts businesses and what steps they should take to remain compliant and financially resilient.

The 9% CIT applies to taxable income above AED 375,000, meaning that businesses will experience a direct reduction in their net profit margins. This is particularly relevant for low-margin industries such as construction, manufacturing, and logistics, where cost efficiency is crucial.

Tax payments must now be factored into cash flow planning, which can be especially challenging for companies with long project cycles and delayed payments, such as real estate developers and contractors.

The introduction of CIT affects existing and future contracts, particularly in industries with long-term service agreements. Companies must ensure that pricing structures factor in tax liabilities to avoid eroding margins.

CIT requires more detailed financial reporting, as taxable income must be calculated based on International Financial Reporting Standards (IFRS). This means companies must:

The UAE corporate tax law introduces transfer pricing (TP) regulations aligned with OECD standards. Companies with related-party transactions must ensure that intercompany pricing is at arm’s length, meaning it must reflect market conditions to prevent tax base erosion.

The new tax system allows businesses to carry forward tax losses, enabling them to offset future taxable income and reduce overall tax liability.

Companies operating in UAE free zones may qualify for a 0% corporate tax rate on specific types of income. However, they must meet strict regulatory conditions to maintain tax-free status.

Tax implications now play a key role in corporate structuring, capital investments, and M&A activities. Increased tax liabilities could influence valuations and financing decisions for companies in capital-intensive industries.

Companies must now allocate budgets for:

The UAE’s tax landscape is evolving rapidly, and businesses must adapt their financial and operational strategies to remain compliant and competitive. While the corporate tax rate remains low compared to many global jurisdictions, the administrative burden and compliance requirements are significant.

To successfully navigate this new era of taxation, businesses should: